Florida has one of the highest rates of uninsured drivers in the country, which makes uninsured motorist coverage one of the most practically important components of any Florida auto insurance policy. For Maitland car accident victims struck by a driver without adequate insurance, UM coverage can be the difference between recovering full compensation and absorbing significant losses out of pocket.

What Uninsured Motorist Coverage Covers in Florida

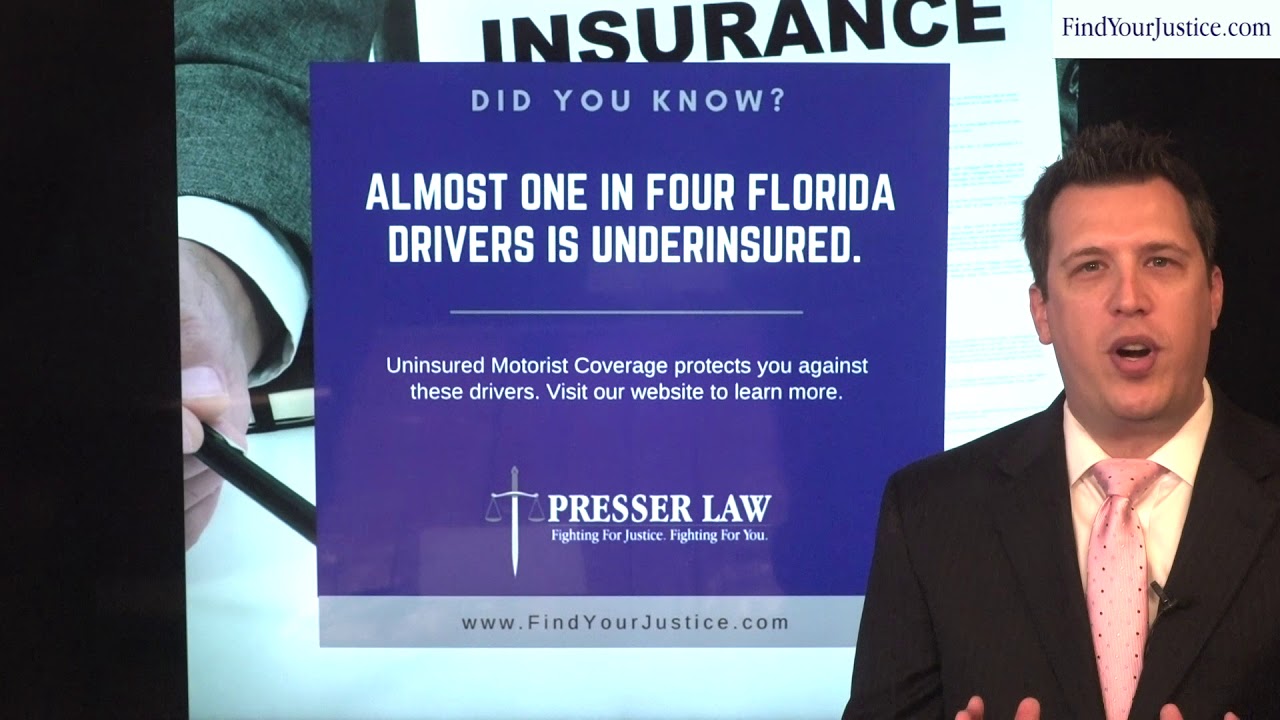

Uninsured motorist coverage, commonly called UM coverage, is a component of your own auto insurance policy that pays for your injuries and losses when the at-fault driver either has no insurance or does not have enough insurance to cover the full extent of your damages. Florida allows drivers to purchase UM coverage in two forms. Uninsured motorist coverage applies when the at-fault driver has no insurance at all. Underinsured motorist coverage applies when the at-fault driver has insurance, but their policy limits are not sufficient to cover your losses.

UM coverage is not required in Florida, but insurers are required to offer it, and policyholders who decline it must do so in writing. Many Florida drivers are unaware of whether they have UM coverage, what their limits are, or what the difference between stacked and non-stacked coverage means for their recovery after an accident.

Stacked vs. Non-Stacked UM Coverage in Florida

Florida allows policyholders to choose between stacked and non-stacked uninsured motorist coverage. Stacked coverage allows the policyholder to combine the UM limits across multiple vehicles on the same policy, effectively multiplying the available coverage. A policy with two vehicles and $100,000 in stacked UM coverage per vehicle provides up to $200,000 in total UM protection. Non-stacked coverage limits recovery to the single-vehicle limit regardless of how many vehicles are on the policy. Stacked coverage costs more but provides substantially greater protection in a serious accident.

How to Make a UM Claim After a Maitland Car Accident

A Maitland car accident lawyer handles UM claims as part of the overall injury case, including the specific procedures that apply when making a claim against your own insurer. UM claims involve your own insurance company, but that does not mean the process is cooperative. Florida insurers handling UM claims are still motivated to minimize the payout, and they evaluate the claim with the same scrutiny they would apply to a third-party claim. The process includes:

- Establishing the at-fault driver’s liability and the extent of your injuries

- Confirming that the at-fault driver was uninsured or underinsured relative to your damages

- Documenting your losses including medical expenses, lost wages, and non-economic damages

- Negotiating with your own insurer for a settlement that reflects the full value of your claim

If your insurer disputes the claim or offers an inadequate settlement, Florida law allows you to pursue arbitration or litigation against your own insurer to recover the UM benefits you are owed.

Why UM Coverage Matters More in Florida Than in Many Other States

Florida is consistently ranked among the states with the highest percentage of uninsured drivers. After a serious crash in Maitland, discovering that the at-fault driver has no insurance leaves an injured person with limited options unless they have their own UM coverage to fall back on. Presser Law, P.A. is a Central Florida personal injury firm representing car accident victims throughout Orange County and the Maitland area, including cases where UM and UIM claims are the primary avenue for recovery.

Protecting Your Recovery Through UM Coverage After a Maitland Crash

If you were injured in a car accident in Maitland by an uninsured or underinsured driver, speaking with a Maitland car accident lawyer about how your UM coverage applies and what steps are required to make that claim is the most direct path to recovering the compensation you deserve.

![[SIMPLE AND EASY] Reason Why You Need to Document the Injury Scene | Personal Injury Attorney](https://www.findyourjustice.com/wp-content/uploads/2025/10/SIMPLE-AND-EASY-Reason-Why-You-Need-to-Document-the-Injury-Scene-Personal-Injury-Attorney.jpg)